February 25, 2017 was when I wrote my last Blog for McKae Properties. Since then I joined to Berkshire Hathaway HomeServices franchiee Drysdale Properties. Drysdale had made many changes and additions to a final point, I could no longer add my commentary to their Monthly newsletter. So “I am Back” as crazy comedian Johnathan Winters exclaimed upon his return from a mental institution on late night Johnny Carson show….if you haven’t seen it do so. He was one crazy fellow!!! https://www.youtube.com/watch?v=4RRpgYKX3JM

In February 2017 we had conditions that are similar to today. Low inventory, interest rates which were low for the time are now lower. Demand for homes remained strong as buyers fought against rising prices only to see them go higher.

So what makes prices go higher and demand to remain strong? What causes the tight inventory?

Let’s go back to school. Remember the law of Supply and Demand? Prices and demand are tied together. More demand and supply does not meet demand…prices go up. More supply and prices go down. Logical.

Now that is the simplistic approach that should be obvious. There is the tie up of homes to the stock market. The stock market goes up, people have more money and they are willing to pay more when houses for sale are in tight supply.

Stock prices rise and home prices rise. They are both asset classes. They both are a source of funds. That is when money is needed for an expense, the owner either sell stocks or bonds or real estate. They both offer liquidity and a store of value.

The largest asset the average American has is their home. When it comes time to cash in their assets the home is sold. Now here comes the trick. Most Americans have bought their homes for life. Business people and those who have a career will not look at a home as a permanent asset. They will look at their home as a cheap alternative to renting that will create store of value and future appreciation, with maybe some tax benefits as interest write off.

Then we have those owners who will look at better alternatives. The 55+ communities have become very popular. Children have moved out and away. The years of sacrificing are over and the need to relax and enjoy the remaining years become something to look at. The growth in 55+ communities have been quite extra ordinary. So has the growth in Senior care centers. Seniors who look at their future with caution would like to have some place to live without the daily needs of cutting grass, replacing broken parts in the house, or fighting with contractors over prices and repairs. The Senior Care centers will appeal to all who seek an alternative and offer price comparisons to the wealth of the buyer. Added to those senior care centers are hospice care. We have all come to face with how to take care of a loved one who can no longer care for themselves. If you haven’t you will! A parent falls and can not care for themselves and are unable to live independently will need some sort of care. The care is not cheap and most do not have Long Term Health Insurance.

How will the care be paid for. Home sale is a natural choice.

So at some point the question of supply of homes will be answered with a Grey Tsunami. The Baby Boom generation, who are the major owners of homes, will sooner of later become the major supplier of home sales. Whether they want to or not, the home will be sold by their children or forced upon them by circumstances.

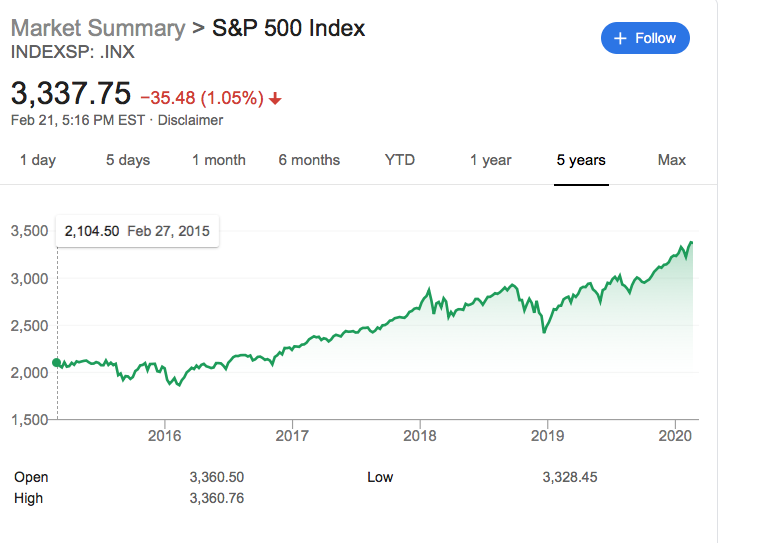

Now let’s go back to the charts. We all know that the stock market has daily swings. The daily swing may pass by until the daily becomes a large decline. It is the law of supply and demand. Prices go too high, sellers reduce offering prices as buyers retreat. The sell off will affect home prices as buyer will feel poorer and they will become less willing to pay up, or over bid on a home for sale.

Whether it is stocks as measured by the S&P or Homes Prices, both will come down to a level the buyer will feel comfortable in making an offer. It is the cycle of that must be followed and every buyer and seller must become aware of.

Begin to look at home prices in the weekly papers and internet news. You will see that homes and stocks march together.

With February coming to an end I will being my monthly commentary on real estate in Atherton, Woodside, Menlo Park, Palo Alto and Portola Valley, with some Redwood City analysis in March.

Until then, please add your comments and questions and send them to gary@mckaeproeprties.com or text to 650-743-7249.

Gary